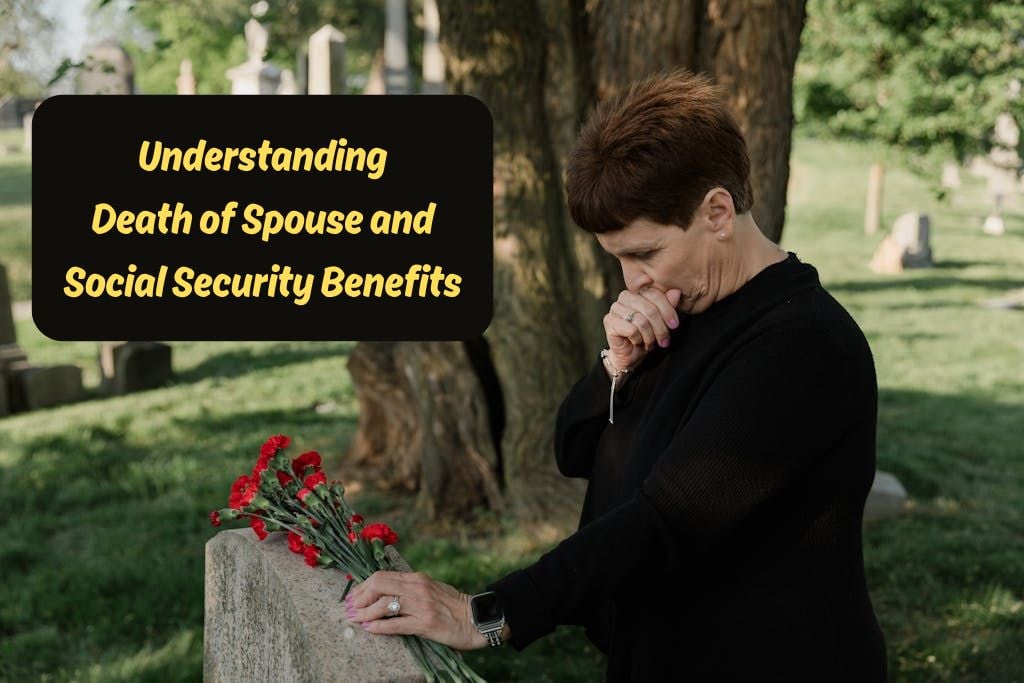

When your spouse dies, the last thing you want to do is sort through government paperwork. But the death of spouse and social security benefits are tied together in ways that catch most people off guard, usually right when they're least prepared to deal with it.

How the Death of Spouse and Social Security Benefits Are Connected?

When a person who has worked and paid into Social Security passes away, their spouse and sometimes other family members may be eligible to receive what are called survivor benefits.

These benefits are designed to provide ongoing financial help for the surviving spouse, especially if they depend on the deceased’s income.

If you are the surviving spouse, you could receive monthly payments based on your late partner’s earnings record. The amount depends on several factors such as your age, your own work record, and whether you are caring for dependent children.

Read Also: Finding Hope and Healing After the Loss of a Spouse

Who Qualifies for Survivor Benefits

Understanding who qualifies is key to managing death of spouse and social security benefits smoothly. Here are the general eligibility rules:

- Age 60 or older

You can start receiving survivor benefits as early as age 60. However, if you start before your full retirement age, your benefits will be reduced. - Disabled widows or widowers

If you are disabled and between ages 50 and 59, you may also qualify. - Caring for a child

If you are caring for a child under age 16 or a disabled child who is receiving Social Security, you may be eligible at any age. - Divorced spouses

Even if you are divorced, you may still receive survivor benefits if your marriage lasted at least 10 years and you have not remarried before age 60.

These benefits can also extend to children and sometimes even dependent parents, depending on the situation.

How Much Can You Receive?

The amount of survivor benefits is based on your late spouse’s lifetime earnings. The higher they earned, the larger the benefit.

The Social Security Administration (SSA) calculates your payment as a percentage of your spouse’s benefit:

- Up to 100% if you are at full retirement age or older.

- About 71–99% if you are between 60 and full retirement age.

- 75% if you are caring for a child under age 16.

It is important to note that you cannot receive both your own Social Security retirement benefit and your spouse’s full benefit at the same time. The SSA will pay whichever amount is higher.

Applying for Survivor Benefits

When dealing with death of spouse and social security benefits, timing and proper documentation are essential.

You cannot apply for survivor benefits online; you must contact the Social Security Administration directly by phone or visit a local office.

You will need documents such as:

- Your spouse’s death certificate.

- Social Security numbers for both of you.

- Birth certificates.

- Marriage certificate.

- Your spouse’s most recent W-2 forms or self-employment tax returns.

The process can feel overwhelming, especially during a time of grief. It may help to ask a trusted family member or advisor to assist you through the paperwork.

Can You Work and Still Receive Benefits?

Yes, you can. However, if you start receiving survivor benefits before reaching your full retirement age, your payments might be reduced if your earnings exceed a certain limit.

Once you reach full retirement age, you can work and earn any amount without affecting your survivor benefits.

For many seniors, this flexibility allows them to gradually transition into retirement while maintaining some financial stability.

Important Considerations for Remarriage

Remarriage can affect your eligibility for survivor benefits.

- If you remarry before age 60, you usually lose the right to claim benefits based on your late spouse’s record.

- However, if you remarry after age 60 (or 50 if disabled), you can still receive those benefits.

This rule often surprises people, so it’s worth discussing with a Social Security representative before making any decisions.

Planning Ahead After Losing a Spouse

Managing life after losing a spouse is not only emotional but also financial. Here are a few steps that can help you regain stability:

- Notify Social Security promptly. This ensures your benefits are updated correctly and prevents overpayments.

- Review your financial needs. Check monthly expenses, insurance, and pension income.

- Seek financial counseling. Many community centers or senior organizations offer free or low-cost advice.

- Consider delaying benefits. If you can, waiting until full retirement age can increase your monthly amount.

The Emotional Side of Financial Loss

Money matters are only one part of the picture. The death of spouse and social security benefits often come with feelings of uncertainty and loneliness.

It is natural to feel overwhelmed. Seeking support from friends, family, or grief counseling groups can make a big difference.

Social Security is meant to ease some of the financial burden, but emotional recovery takes time. Connecting with others who have experienced a similar loss can help you heal while you learn to manage your new financial situation.

Final Thoughts

The death of spouse and social security benefits may seem complicated, but understanding the basics can bring peace of mind.

By knowing your rights, gathering the right documents, and planning carefully, you can make sure you receive the benefits you are entitled to.

Read also: When Should You Retire and Take Social Security? A Guide for Seniors

Most importantly, remember that these benefits exist to support you during one of life’s hardest transitions. You are not alone; help and guidance are available whenever you need them.